Understanding the mechanism of online payment processing and the art of payment orchestration is a bit tricky. But there is one solid rule – Corefy is always here to help.

Aiming to help you sort things out, we launch a multi-part column by our Lead Product Architect Ivan. He will kindly share tips on how to untangle the knot of e-commerce, streamline all payments, and boost your profit. So, ladies and gentlemen, sit back and grab the insights.

.png)

Commerce: how sales are made offline

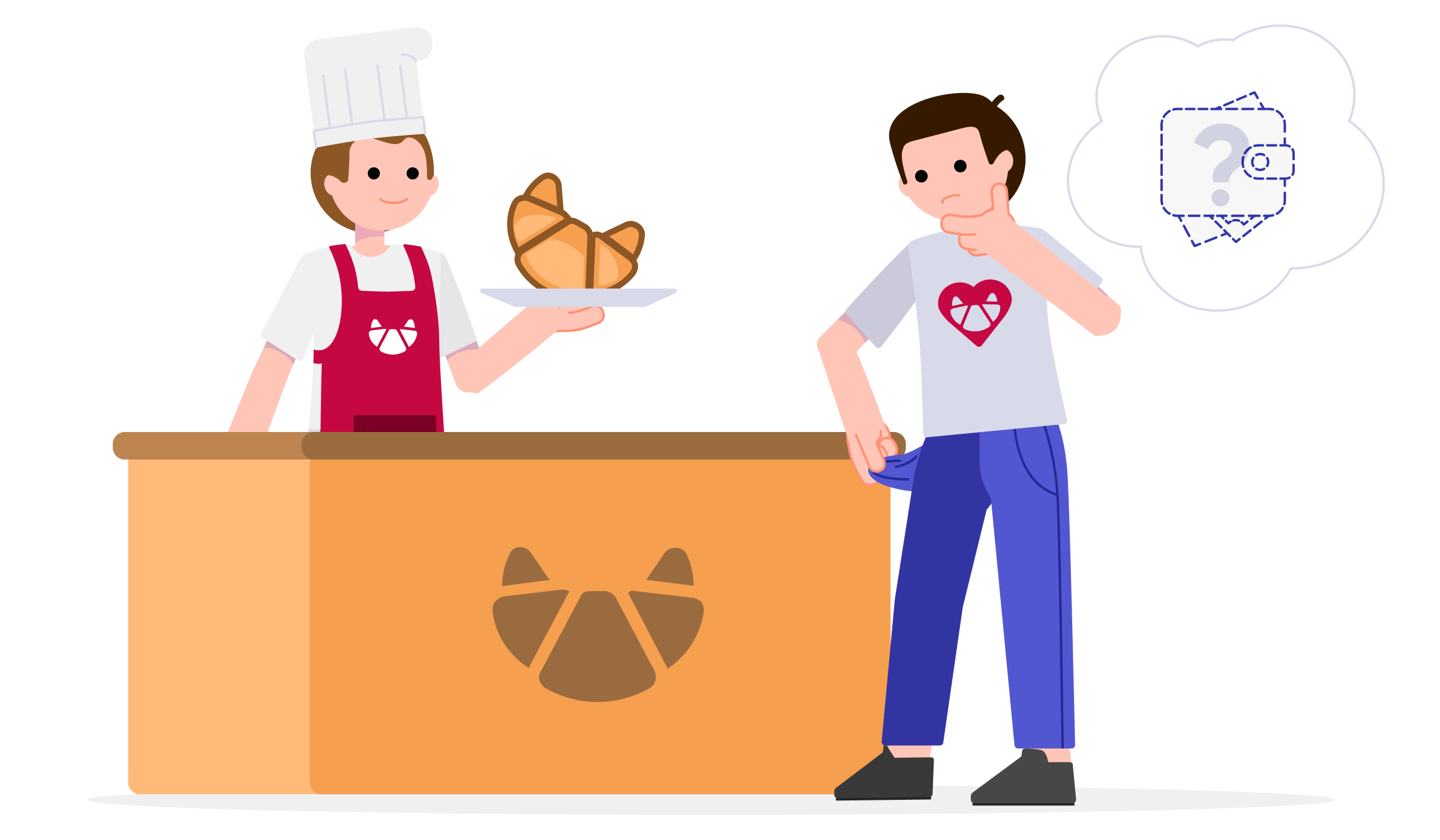

We will be assisted by Mr. Baker, who bakes and sells delicious croissants and Mr. Eater – a croissant lover. So, Mr. Eater comes to Mr. Baker's shop and wants to buy a croissant. It costs 20 UAH. He gives this money to Mr. Baker and gets the expected croissant. Everything works perfectly – croissants are baked, Mr. Eater buys them, and Mr. Baker receives his 20 UAH. The scheme breaks down when Mr. Eater forgets his wallet at home, comes to Mr. Baker, and realises that he doesn't have 20 UAH, only a bank card. What shall they do?

Mr. Baker has no tools to accept cashless payments. He can only register Mr. Eater in a debt book, as some people do in small village shops, or give him a croissant as a gift. But if such situations occur frequently, Mr. Baker would experience certain inconveniences or losses. Therefore, he'll most likely refuse, and upset Mr. Eater will go to a competitor's bakery, where he can pay with his bank card. Chances are, he'll never come back to Mr. Baker even with cash. For Mr. Baker, it means a loss of a loyal customer. How can he cope with it? He starts wondering how to carry out sales without cash.

Cashless payments

Looking at his competitors' businesses, Mr. Baker notices that they use POS terminals in their bakeries. And he, probably, also paid for purchases via such terminals more than once.

After installing a POS system in his bakery, he explores the payment services market and comes to a bank willing to open an account. The bank allows Mr. Baker to deposit and withdraw money from it. They will also give him a "key" – his account credentials and a POS terminal directly connected with the bank. So, when Mr. Eater comes without cash but has a bank card or some gadget supporting the NFC technology, he'll be able to pay via the terminal. The payment will end up in Mr. Baker's account, but not for free. He'll pay fees for using the POS terminal and for each transaction.

Implementing the additional payment method allows Mr. Baker to save more clients and boost sales. And all those clients who could not buy a croissant before because it was inconvenient for them to carry cash will now be able to do it. As the number of purchases grows, so does Mr. Baker's profit. Thus, the expenses on fees will be reasonable.

E-commerce: how the Internet changed sales

The croissants are baked, customers buy them, and the money is deposited to Mr. Baker's bank account. What can go wrong? This scheme is short-lived if a business decides to expand and start making online sales.

Being a savvy businessman, Mr. Baker decides to create an online store for selling his croissants. From now on, his customers don't even have to leave their homes to get croissants. They can open his website, choose croissants, and pay. But how? There are several ways to do it.

Online payments

Mr. Baker can indicate his bank card number in the "Payment and Delivery" section, and when Mr. Eater chooses croissants, he'll see something like "Send so-and-so many UAH to this card." But this method is not secure. Choosing it, you make an advanced payment and take all the risks in case of a mistake or not getting the croissants. Moreover, this method is inconvenient for legal entities. I.e. if a company decides to buy a batch of croissants for their staff, they'll prefer the bakery where they can pay officially to a bank account. Thus, Mr. Baker can add an opportunity to pay via a transfer to his bank account.

Having both methods in stock might work until the tax officer comes to Mr. Baker someday and asks: "Darling, where did you get such a flow of money on your bank account?". The scheme is illegal since any commercial activity must be under the supervision of the tax authorities.

Accordingly, we will not consider these schemes. Let's pay attention to another: Mr. Baker can go to the bank and say, "Guys, you gave me a POS terminal for offline payments. Can you offer me some tool for paying in the virtual world?" The problem is that some banks might be incapable of meeting his needs because of the outdated technologies they use. They might be incompatible with the APIs and all the stuff we do in IT companies.

Payment service providers

Some guys on the market still integrate the old bank APIs and other payment providers. They may be called PSP, payment service provider, vendor, payment system, and financial institution – different terms meaning the same thing. Providers are, in fact, similar to banks. They provide accounts for depositing and withdrawing money.

Probably the most widespread payment provider in Ukraine is LiqPay. Therefore, Mr. Baker might consider it a relevant online payment tool for his bakery website. So, LiqPay will open an account for him. And as Mr. Baker for LiqPay is a merchant, it'll be called a merchant account. Mr. Baker gets access to this account and shares the access with the specialists involved with his site development to integrate LiqPay.

Once the integration is live, Mr. Eater visits Mr. Baker's website, chooses croissants, clicks "Buy", and lands on a payment page. In most cases, there should be a form where customers enter their card number, CVV, and expiration date. Or, they may opt for Google Pay or Apple Pay and then just press the "PAY" button without entering any payment data. After that, the corresponding request is sent to LiqPay. Through interaction with international payment systems, LiqPay withdraws money from Mr. Eater's card, which he used on the checkout page. The money goes to Mr. Baker's account on LiqPay. Later, he can withdraw this money to his bank account. Voila!

This scheme requires only one developer; if Mr. Baker is a talented and intelligent guy, he can even do it himself because the integration with LiqPay is quite simple.

So, everything works fine: croissants are being bought, payments are made online and offline, Mr. Baker is satisfied, and sales are growing sky-high.

.png)

Unfortunately, this scheme of accepting online payments is not fail-proof, and there are weak points that can let Mr. Baker down. We'll inspect all the blind spots and ways to avoid them in the next part of our series. Stay tuned!

.png)

.png)

.png)