There are many cogs and gears in the payment lifecycle, and just as many terms are used to describe them. If you are in the dark on certain points, you might stumble upon various concepts and ideas. One common point of confusion is the difference between the typical payment process stakeholders — payment aggregators and facilitators. They are sometimes used interchangeably but, in reality, connote different concepts.

Keep calm. We are here to assist and enhance your knowledge of the payment process. Let's determine the similarities and differences between payment facilitators and aggregators.

Payment processing: who is involved?

To better understand the meaning of each concept, let's clarify who is involved in the processing of a transaction. Here are the four pillars that make transaction processing possible:

- Card issuer – a bank that issued a buyer's card);

- Acquirer – a bank that processes payments for the merchant);

- Cardholder – a buyer who pays for a product or service);

- Merchant – a business that sells goods and accepts card payments).

Now let's find out the difference between the elements that work behind the scenes of each payment.

What is a payment facilitator?

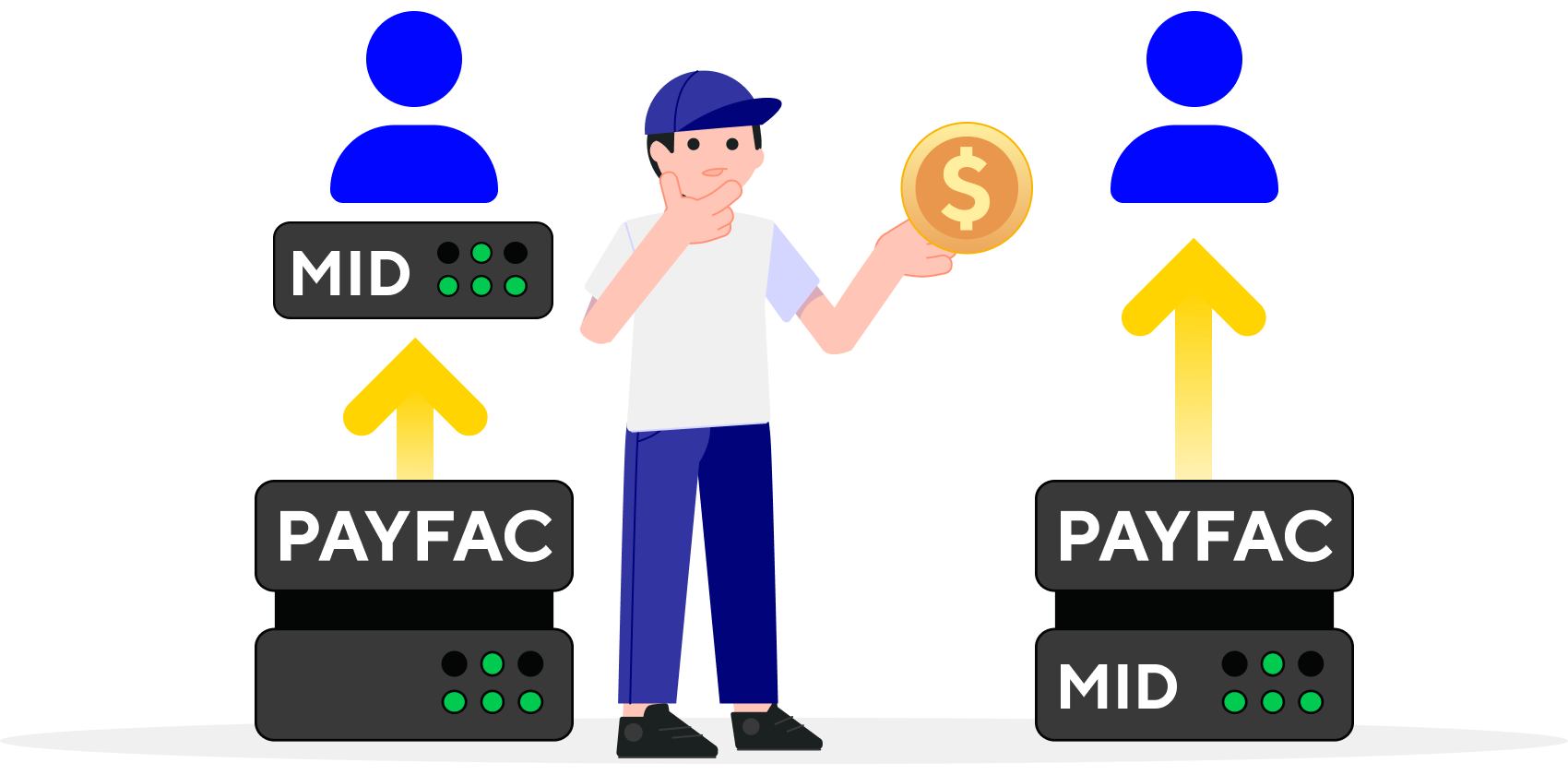

A payment facilitator, often abbreviated as PayFac, is a financial services provider that simplifies the process of accepting payments for smaller merchants or businesses. Payment facilitators assume a more direct role in payment processing, unlike payment aggregators, which act as intermediaries between merchants and acquiring banks.

A payfac is the owner of a master merchant identification number that registers merchants as sub-merchants and enables their payment acceptance. When you start accepting payments online, you need a merchant account from a payment facilitator with sufficient infrastructure and proper compliance.

How does payfac work?

In a nutshell, payfacs onboard merchants as sub-merchants under their master MID, thus helping them with payment processing.

It used to take weeks to get an account for merchants directly, but then payfacs came around and simplified the process by creating a sub-merchant platform. It involves a payment facilitator who has been pre-approved for one master merchant account with an acquirer. Payfacs can then sign up merchants underneath their master account as sub-merchants, thus expediting the enrolment process.

This model is quite appealing to merchants since the risk lies on payment facilitators, as they hold the master account. Merchants can still get individual merchant accounts, but it can be cumbersome.

Why choose the payfac model?

- Quick start & fast onboarding. Getting started is quicker because fewer parties are involved in the process, so you can start accepting payments almost at once.

- Better control. You do not depend on a third party to provide merchant support and control the level of service that you provide to your customers.

- PCI DSS compliance. You can benefit from your master merchant's PCI compliance and remove this burden from your business.

- Increased revenue potential. Since you own more control of the process, you will often have a higher revenue share with your payments partner, boosting your bottom-line profits.

- Fraud-control. This burden is also taken care of for you when using a payfac.

Disadvantages of payment facilitators

Although payment facilitators offer a convenient and speedy solution for processing payments, they may not necessarily be the optimal choice for all businesses. Using a payment facilitator comes with certain drawbacks:

- Customisation. Payfacs generally have a standard set of services, leaving little room for personalisation.

- Control. Merchants have less control over their transaction processing, such as the security measures and fraud detection systems in place.

- Dependence. Relying on a single provider for all payments can be risky due to disruptions or ceased operations.

What is a payment aggregator?

A payment aggregator is a type of financial service provider that facilitates online transactions by acting as an intermediary between merchants (sellers) and customers. Instead of each individual merchant needing to set up their own merchant account with a bank to accept payments, they can use the services of a payment aggregator.

It allows for working not only with cash-on-delivery but also with popular systems like Visa or MasterCard, virtual currencies, and payment systems. Currently, a payment aggregator is the only system that allows you to organise electronic settlements easily and quickly. That makes it necessary for everyone who does business in the virtual space.

How does it work?

Imagine a purchaser placing an order in an online store. The purchaser chooses the desired payment method on the payment page and enters their payment details. The online store's payment aggregator then checks the information and processes the transaction. After the payment is processed, the aggregator returns the buyer to the website of the online store and reports the operation's results to the online store server.

Advantages of payment aggregators

- Versatility. They unify all possible payment methods into one and eliminate the need to connect each separately.

- Time-efficiency. Payments take place in seconds.

- Cost-effectiveness. The commission for paying with a universal payment aggregator is often lower than paying through a specific payment system.

- Reports. Merchants can monitor and analyse transaction data according to various criteria.

- Ease of use. The payment interface is simple and intuitive.

Disadvantages of payment aggregators

- Working with payment aggregators is relevant for small and medium businesses with low transaction volumes. As transaction volumes increase, the operational costs of using a merchant aggregator can become significant, reducing profit.

- There also can be account holds due to the considerable risks payment aggregators assume on behalf of their clients or sub-merchants. A hold can last from 24 hours to even a month in certain cases.

- Funds are usually settled to merchants within 24-48 days, and instant settlements can take as little as 15 minutes. However, if there are any issues with fund capture, it can cause settlement delays of up to a month.

- Payment aggregators set rigid limits on the number of allowed transactions, which may be acceptable for small businesses but can interfere with the development of larger projects.

Both aggregators and facilitators offer similar benefits from the end user's perspective. Aggregators, due to their simpler model, usually offer less expensive processing for a low number of transactions. However, they are not the best option for organisations with high transaction volumes.

Difference between payment aggregators and payment facilitators

A payment aggregator acts as an intermediary between merchants and acquiring banks, enabling multiple merchants to accept payments through a single merchant account. They process transactions on behalf of merchants, deduct fees, and then disburse funds to individual merchant accounts. In contrast, a payment facilitator directly integrates smaller merchants onto its platform, providing them with sub-merchant accounts under its master merchant account and handling payment processing, risk management, and fund disbursement.

Payment facilitator vs aggregator: how to choose?

Without looking under the hood, these services do not differ from each other fundamentally. However, when choosing a specific payment service provider for your business, rely on the following five points:

- Cost of the commission.

- List of supported payment methods: cards, terminals, virtual currencies.

- Level of technical support service.

- Supported types of business (some aggregators serve small businesses well but can malfunction with the large ones, and vice versa).

- Proper customer support to resolve issues quickly. This option is essential for small businesses, as customers appreciate the level of service and the ability to contact support at the first need.

We at Corefy are ready to help you make your payment processing as smooth as possible with our feature-rich payment orchestration platform. It suits businesses of all types and allows them to start accepting payments and making payouts hassle-free across the globe with ultimate efficiency and safety.

Feel free to contact us and find out more about our solution, which best suits your business model.